#6: Germany’s economy is on the brink

Higher energy prices coupled with weaker real demand points to a weak period over the next 6 months for the German economy.

Summary:

Weakness in German industrial activity is likely to get worse over the next few months

Actual production could remain elevated relative to new orders however as Companies look to get through existing backlogs

Squeeze on real incomes have hurt retail spending

There could be a potential boost to spending due to higher savings following the winter

Despite the attention the US economy has gained recently, it’s really some parts of Europe including the UK that have shown the first signs of breaking.

This would be unthinkable in the US!

However, it is the German economy that I’ve found most fascinating recently.

The combination of a stalling Chinese economy on the back of its zero-covid policy, the energy crisis and Russia’s war on Ukraine have caused significant damage already.

The following points stood out:

Goods producers reported the steepest drop in output since May 2020, whilst also noting a deepening decline in new orders, as conditions across the sector worsened amid growing concerns about the economic outlook and high energy costs.

There was some alleviation of overall costs pressures, however, with falling demand for materials and an associated easing of supply-chain constraints contributing to a slowdown in input price inflation to a 21-month low.

Factory employment meanwhile continued to defy the broader downturn in conditions, as firms reported filling vacancies amid efforts to clear backlogs of work.

Easing supply bottlenecks were evidenced by a drop in the incidence of delays on purchases to the lowest since August 2020.

The key points were:

Where a decrease in business activity was recorded, surveyed firms often commented on a weakening of underlying demand.

Inflows of new work fell for a fifth successive month during October. The rate of decline, although less marked than in September, was still faster than at any other time since February 2021.

A further notable – albeit slightly slower – drop in new export business was also registered.

In October, services firms faced a rate of input price inflation that was the quickest for four months and one of the highest on record (since 1997). Alongside high energy costs, many firms noted an increase in wage bills, as well as pressure from rising interest rates.

Chart 1: German PMIs continue to signal a deteriorating economy

Source: VKMacro, Koyfin

I tend to use real M1 growth (narrow money) in the Eurozone as a leading indicator of domestic demand. It tends to lead the manufacturing PMIs by 6 months. The indication from real M1 growth is pretty poor, it shows German PMIs could fall as low as 40 in coming months.

Chart 2: Eurozone M1 growth points to a more severe environment for German manufacturers

Source: VKMacro, Koyfin

Why do I care about the PMIs so much? Well, as I say they’re the best real time indicators of growth and inflation that we get. The manufacturing PMI is also highly correlated to both new factory orders and industrial production as shown by the chart below.

Chart 3: We typically see a tight relationship between PMIs and German manufacturing and factory data

Source: VKMacro, Koyfin

As chart 3 shows, manufacturing new orders peaked in July 2021 and have slowly decreased ever since. Given the weakness in global goods demand due the shift from goods to services, as well as a real income squeeze, it’s hard to see this reversing.

Digging a bit deeper into new factory orders, weakness can be seen in both domestic and external new orders which are both shrinking on a 3m/3m basis.

Chart 4: Weaker factory orders can be seen in both domestic and foreign orders

Source: VKMacro, Destatis

The non-domestic orders bit is likely being driven by the weakness in China as they are the largest contributor to export growth. To provide some more context, the FT reports that:

Additionally, Germany has also become reliant on Chinese goods as part of its supply chain. China is now the largest import destination for Germany, larger than any of its European partners and the US. This can be seen in the chart below.

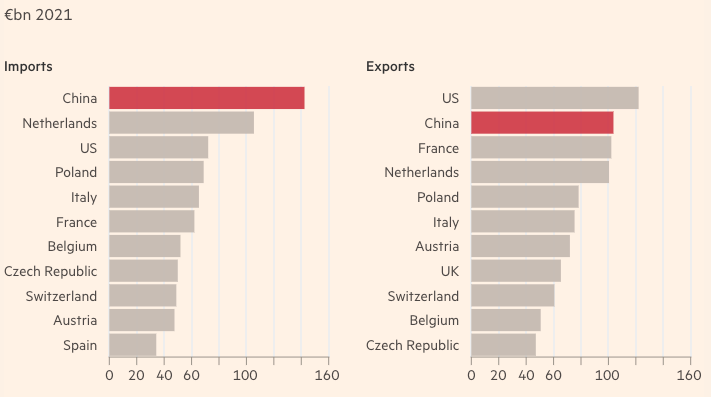

Chart 5: China has become a major destination for German exports

Source: Financial Times

The combination of slower sales growth into China and the longer time taken to receive Chinese goods are both directly due to China’s zero-covid policies.

The other side to this is the impact on domestic new factory orders. The rapid increase in wholesale electricity costs due to gas shortages are already crippling German industry. The scale of the impact can be seen by looking at German producer prices which recently rose by 45.8% Y/Y. Energy prices as a whole were up by 132.2% compared to September 2021. The strong rise in energy prices was mainly due to the large price increases for natural gas (distribution), which was up by 192.4%, and for electricity (+158.3%).

Removing the impact of direct energy price increases however, PPI still rose by 14% relative to September last year, which is incredibly high.

Sure, a lot of this will also be directly driven by higher energy prices such as the price increases of basic chemicals, fertilisers and nitrogen compounds, which increased by 33.5% Y/Y. Other examples include the increases observed in the prices of fertilisers and nitrogen compounds (+113.5 %). The price of ammoniac, which is used for the production of fertilisers, was up 208.7%.

Chart 6: German Producer Prices have reached all time highs on the back of higher energy prices

Source: VKMacro, Destatis

It’s worth remembering that natural gas is the single most important source of energy for Europe’s industrial companies. But gas is also an important feedstock, used in the chemicals and fertiliser industries. In total, industry consumes about 27-28 per cent of the bloc’s total supply, according to Anouk Honoré, deputy director of the gas research programme at the Oxford Institute for Energy Studies.

Chart 7: European industry’s reliance on natural gas

Source: Financial Times

Some industrial companies have announced they plan to ration their usage of natural gas over the winter and others have already stated their intentions to switch to oil or coal as well. For instance, the FT reports that:

Carmaker Volkswagen is running power plants in Wolfsburg, its largest site, with coal for the next two winters, instead of switching to gas as planned as part of its decarbonisation efforts.

thyssenkrupp AG, the German industrial engineering and steel production multinational conglomerate reported in August that they have already designed ‘action plans’ for the winter where shortages are likely to be more severe:

The first and foremost, and as a direct impact of the world, we also are confronted with uncertainty for natural gas supply. Though only accounting for 10% of the energy consumed in the group clearly a crucial topic also for our Steel segment. Here, we took early action and defined action plans for different scenarios of potential gas shortages, and ensure that operations can be maintained most efficiently and damages of our aggregates avoided.

They also discussed the usage of LNG in their steel production process but discussed that adjustments to their existing processes would be required to transition effectively.

Linde, Germany’s largest listed company and producer of industrial gases has talked about how they ‘acted early’ due to their view that inflation would not be transitory. One of the things they did to draw upon the expertise their Latin American team had acquired by working in high inflationary environments.

It’s also clear that some businesses are more impacted than others. The predominant impact falls on businesses that operate in the production of chemical products, metal production and processing, coking plant and mineral oil processing, and the production of glass, glassware, ceramics, paper and cardboard.

The impact of the energy crisis can be seen by looking at industrial production within the energy intensive industries mentioned above relative to the rest.

Chart 8: Energy intensive industries have already begun to cut back production in the face of higher gas prices

Source: VKMacro, Destatis

Chart 8 shows that while overall industrial production is growing at c. 1% on a 3m/3m basis, production at energy intensive industries has fallen by almost 5% over the same period. We should expect this trend to continue over the coming months as Germany looks to cut gas usage by almost 20% over the winter.

As mentioned in the PMIs, despite the weakness in new orders, German manufacturers continue hiring new workers to clear existing backlogs. Destatis tracks the stock manufacturing backlogs which remain elevated due to supply chain issues.

Chart 9: Supply chain issues have resulted in the stock of manufacturing backlogs reaching all time highs

Source: VKMacro, Destatis

The IFO institute published a shortage indicator survey which showed that approximately 65.8% of the industrial enterprises included stated in September 2022 that they were affected by impediments to production caused by scarce raw materials and intermediate products. The indicator shows the percentage of enterprises that answered yes to the question about impediments to production because of raw material or intermediate product shortages.

The direct result of the scale of backlogs is that industrial production, and therefore employment can remain elevated while overall demand drops off. This could have an impact on monetary policy as it prevents the labour market from loosening in the face of higher rates.

Chart 10 shows how backlogs have evolved relative to new orders and industrial production. As the stock of orders comprises all new orders received by the end of the reference month which have neither led to any turnover nor been cancelled by that time. As new orders have risen more strongly than production, the stock of orders in manufacturing has increased considerably.

Chart 10: Industrial production could remain strong despite lower new orders due to elevated backlogs

Source: VKMacro, Destatis

Moving away from manufacturing, and German industrial activity, the IFO institute also provides a bit more granularity into how the rest of the economy is performing.

Chart 11: The IFO survey shows widespread weakness across the German economy, with the retail sector particularly being hard hit

Source: VKMacro, IFO Institute

The biggest areas of concern are within the retail sector as negative real income growth has hurt the purchasing power of the German consumer. I highlighted the collapse of German consumer confidence in a previous post, but it continues to make new lows.

Chart 12: German consumer confidence has fallen off a cliff hinting to weaker spending going forward

Source: VKMacro, Koyfin

GfK, the company that conducts the survey has talked about how German consumers have increased the amount they save in order to build up a buffer. The key bit to highlight from the recent report is below:

The sharp increase in the propensity to save this month means that the consumer sentiment is continuing its steep descent. It has once again hit a new record low," explains Rolf Bürkl, GfK consumer expert. "The fear of significantly higher energy costs in the coming months is forcing many households to take precautions and put money aside for future energy bills. This is further dampening the consumer sentiment, as in return there are fewer financial resources available for consumption elsewhere.

We can see the weakness in consumer confidence and the IFO retail sector in retail sales. German retail sales have been sluggish recently, growing at 0% over the last 3 months in real terms. This is distinctively different from previous periods of German economic weakness such as 2018 where retail sales were still growing.

Chart 13: German real retail sales have been weak ever since Russia’s war on Ukraine

Source: VKMacro, Destatis

Until we see a period of lower inflation following an easing of the European gas crisis it’s hard to see this trend materially changing. We should expect to see higher savings ratios for German consumers. Typically, the German households tends to save c. 10% of their income, and I’d expect to see numbers come in higher than this over the coming quarters.

Its worth noting that most of what I’ve described over this post is well understood by the market, so this post isn’t an instruction to go and short the EUR or the DAX.

It is however important to understand existing dynamics in order to think about where opportunities may exist going forward. For instance, higher German savings now, may lead to higher spending once European energy prices normalise. In addition, already discounted German manufactures may be good long ideas over 2023 if energy rationing comes to an end, especially relative to their US competitors.

Summary:

Weakness in German industrial activity is likely to get worse over the next few months

Actual production could remain elevated relative to new orders however as Companies look to get through existing backlogs

Squeeze on real incomes have hurt retail spending

There could be a potential boost to spending due to higher savings following the winter

Thanks,

VKMacro

expect germany to adapt well in the mid-term. they are subsidizing 70% of industrial use (based on past averages) with other 30% based on pricing of more expensive LNG imports. biggest risk is the allowed 'free market' trading of subsidized gas, which could mean some in supply chain could become traders instead of producers critical within the chain.

long-term is a wildcard based on putin...his disappearance could mean whatever gas infrastructure still functional could flow freely as war reparations.