#1: An update on UK Macro...

Despite Government support, the Bank of England remains in between a rock and a hard place.

Summary:

The outlook for the UK continues to deteriorate

The Bank of England are stuck between a rock and a hard place as they are forced to balance between weakness and high headline inflation coupled with labour shortages.

UK retailers and banks remain good shorting opportunities over a cyclical horizon.

It’s fairly concensus at this point that the UK economy is struggling. In fact, I’d argue that prior to the Treasury’s recent policy measures which aim to offset future rises in energy bills, a recession was all but certain.

The most obvious example of a slowing economy is the most recent monthly GDP estimates from the ONS where the UK economy contracted by 0.3% in April, following a 0.1% decrease in March.

Sources: ONS, VKMacro

However, the recent print was also heavily distorted to the downside by the end of Test and Trace and Covid-19 vaccine programme which contributed c. 0.5% of the 0.3% fall. The full breakdown of key contributors can be seen in Chart 2 below. Overall, a noisy report and while we shouldn’t read too much into one report, it’s hard to find anything to be encouraged by.

Chart 2: Breakdown of UK’s May GDP growth

Source: ONS

The most recent PMI’s provide further clarity as to how the economy is fairing. I’ve provided some of the more salient points from the most recent reports below (emphasis mine).

Sources: Koyfin, VKMacro

The most recent Manufacturing PMI came in at 54.6 in May, down from 55.8 in April. The report showed that manufacturing output increased at the slowest pace since October 2021. We also see that demand for consumer goods industry was especially weak, with production falling for the first time in 15 months.

“May saw the weakest increase in new work received during the current 16-month sequence of expansion. Supply chain issues, subdued client confidence, signs of economic slowdown and reduced export order intakes all stymied new order growth. New orders declined in both the consumer and intermediate goods sectors. The downturn in the former also reflected the impact on consumer demand of the current cost of living crisis.

Input cost inflation stayed substantial in May, easing from April's near-survey record high. Chemicals, energy, food, freight, fuels, gas, metals, oil, plastics, polymers, timber, and transportation (air, land and sea) were all reported as being up in price.

Business optimism dipped to a 17-month low and weaker demand growth led to surplus production, meaning warehouse stock levels are rising.”

Overall Services PMI reading of 53.4 in May, down from 58.9 in April.

Business Activity Index pointed to the slowest rise in output volumes since the current period of expansion began 15 months ago. Travel, leisure and entertainment was the main exception, with hospitality businesses widely commenting on strong consumer demand due to the removal of pandemic restrictions.

The rate of new business expansion was the weakest since December 2021. Some service providers noted that steep rises in their prices charged had exerted a negative influence on demand, while others suggested that supply shortages had constrained customer spending.

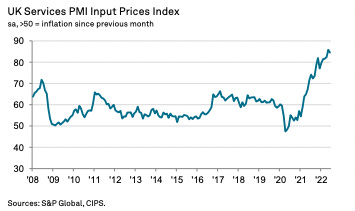

The rate of cost inflation was the steepest since the survey began in July 1996. Around 70% of the survey panel reported a rise in their average costs since April, while only 1% noted a decline.

Chart 4: Input prices within the Services industry continue to rise at a record pace

The key takeaway is that growth is clearly decelerating across the board, with new orders declining within the Manufacturing sector.

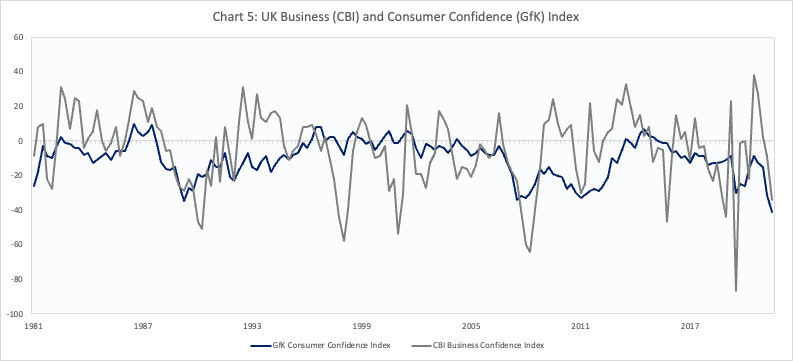

The increase in input prices remains at record highs. This is clearly a toxic combination and has resulted in business expectations to deteriorate rapidly. The chart below shows the striking decline in both business and consumer confidence in particular which is at all-time lows.

Sources: Koyfin, VKMacro

The combination of a rapidly slowing economy, coupled with increasing prices puts the Bank of England in a precarious position which they’ve talked about at length during recent speeches.

The dilemma facing the Bank of England is that they can’t be seen to be taking the pressure off inflation at a time when headline CPI is at 9.1% (YoY) and expected to rise further. The Bank has outlined their fear of “second-round effects” whereby workers demand higher wage increases which further prevents inflation from normalising.

Huw Pill outlined the conflicting risks during his speech on the 24th of May. He says that:

On the one hand, there is a danger that the current high level of inflation becomes embedded in wage and price setting behaviour, imparting greater persistence to the upside deviation of inflation from target in the coming years.

On the other hand, the squeeze on real household incomes coming from higher energy and goods prices threatens to weigh heavily on demand, activity and employment, potentially adding to the undershoot of the inflation target forecast by the MPC at a three-year horizon.

Huw is one of the more prominent doves on the MPC. He articulates his rationale for a steadier approach to rising interest rates due to the fact that that he doubts that:

BOE know enough about: (1) about the state of the economy; (2) about key features of the economy’s structure and behaviour; (3) about the intrinsic properties of inflation dynamics; or (4) about the monetary policy transmission mechanism, to be able to use monetary policy to ‘fine tune’ economic and price developments

I think given the complexity of the current situation, and the array of moving parts, coupled with the idiosyncrasies within the UK labour market (more on this soon), this approach is justified.

In my view, the UK’s inflation problem can be split up into the following ways.

Impact of international food and energy prices rises (including impact of Russia’s war on Ukraine)

On commodity prices, the Bank acknowledges there is little they can do with monetary policy to help.

The main way higher oil and gas prices impact consumers is via higher transport costs and higher energy bills (heating etc.).

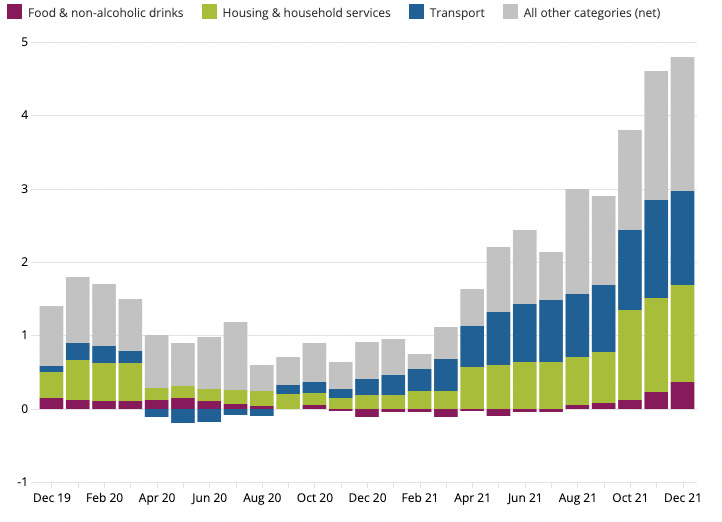

Chart 6: Contributions to the CPIH 12-month inflation rate, UK, December 2019 to December 2021

Source: ONS

The Bank said that the full impact of higher wholesale gas prices is to come in effect in October during the next hike to the energy price cap. The Resolution Foundation estimates that based on an increase of a typical annual dual fuel bill to £2,500, more than 5 million households would find themselves in fuel stress (defined as spending 10% or more of their household budgets on energy bills).

Below is another chart via the Resolution Foundation showing the incremental impact of each increase in the fuel cap and its impact on the % of households in fuel stress. This chart helps to show the scale of the impact that these cost increases will have on households.

Chart 7: % of households in fuel stress by income deciles

Source: Resolution Foundation

Given this impact, doing nothing was just not an option for the government as this would have meant almost a certain recession come October (if not before).

In May, OFGEM confirmed that the hike was likely to increase the energy price cap to c. £2,800. The Chancellor of the Exchequer responded by announcing a series of policy measures aimed at protecting the consumer. These were:

Payments of £650, made over two lump-sum grants, to over 8 million households on means-tested benefits;

An additional £300 on top of the usual Winter Fuel Payment this winter, going to all pensioner households;

An additional £150 to around 6 million people who receive a disability benefit;

Doubling the discount on all households’ electricity bills due this autumn to £400, and:

An additional £500 million for the Household Support Fund from October 2022.

These come on top of measures already announced earlier this year, namely:

A £200 rebate on electricity bills, due to take effect this autumn, and a £150 Council Tax rebate for households in Bands A to D, both announced in February 2022, and:

An increase in the National Insurance threshold from £9,880 to £12,570 in July and a 5p cut to Fuel Duty rates announced in the Spring Statement.

Of the £15 billion of new measures, almost double that announced earlier in the year, twice as much will go to households in the bottom half of the income distribution as the top half. This fills the gaping hole left by the focus of previous support on middle- and higher-income households, and means that all measures announced this year to support households will in effect offset 82 per cent of the rise in households’ energy costs in 2022-23, rising to over 90 per cent for poorer households. Because 2022-23 has also seen major tax rises for higher income households, the effect of all tax and benefit policies coming into play this year is highly progressive: households in the bottom quintile will gain on average £1,195, compared to £799 for households in the middle quintile, while the top quintile on average loses £456.

But it’s important to remember that this is just one part of the burden households are facing. Transportation, food, housing and other non-discretionary items have still gone up markedly. The ONS reported in April a survey of how different groups in the population have been affected by an increase in their cost of living. The key findings were:

Around 9 in 10 (87%) adults reported an increase in their cost of living over the previous month in March 2022 (16 to 27 March 2022), an increase of 25 percentage points compared with around 6 in 10 (62%) adults in November 2021 (3 to 14 November 2021).

Nearly a quarter (23%) of adults reported that it was very difficult or difficult to pay their usual household bills in the last month, compared with a year ago, in March 2022 (16 to 27 March 2022); an increase from 17% in November 2021 (3 to 14 November 2021).

Focusing on the latest period, among those who pay energy bills, around 4 in 10 (43%) reported that it was very or somewhat difficult to afford their energy bills in March 2022 (16 to 27 March 2022).

Of adults currently paying off a mortgage and/or loan, or rent, or shared ownership, 30% reported that it was very or somewhat difficult to afford housing costs, and 3% claimed to be behind on rent or mortgage payments, in March 2022 (16 to 27 March 2022).

Among all adults, 17% reported borrowing more money or using more credit than they did a year ago, in March 2022 (16 to 27 March 2022).

Among all adults, 43% reported that they would not be able to save money in the next 12 months, in March 2022 (16 to 27 March 2022); this is the highest this percentage has been since this question was first asked in March 2020 (27 March to 6 April 2020).

The higher price of petrol/ diesel has resulted transport related costs contributed c. 17% of the year-on-year change in inflation in May. It’s clear that this shock is a material tightening of conditions for households, and lowers the outlook for future spending. For instance, when looking at the GfK Consumer Confidence survey (chart 5 above), the “Major Purchase” sub-index has fallen by 3 points since April and 30 points since last year to -35.

So what reasons have the BOE given for raising rates during this time? Well, it all centres around labour market tightness.

Domestic Labour markets

The domestic labour market is where the Bank of England states they are a bit more concerned about the “second-round effects” as workers demand higher wages to compensate for the higher cost of living. The other risk they see is the risk of longer-term inflation expectations getting unanchored which materially changes the behaviour of participants within the economy such as front-loading demand which further exacerbates the inflation problem. The strength of the labour market has been surprising, by Huw Pill’s own admission where he states that:

Momentum in the labour market continues to be both strong, and stronger than previously expected. Vacancies are at historical highs. Redundancies are at historical lows. The MPC forecasts the unemployment rate will fall to 3.6% in Q2 – the lowest level seen for almost fifty years. […] Bank staff estimates of underlying wage growth continue to strengthen, and are already running at rates above those normally deemed consistent with the inflation target.

One of the main reasons for the tightness in the labour markets is the shrinking of the work-force since Covid began. The Bank estimates that this number could be as large as half a million people. Michael Saunders, another MPC member, discusses the impact of this and how surprising it has been during a speech he gave in May where he states:

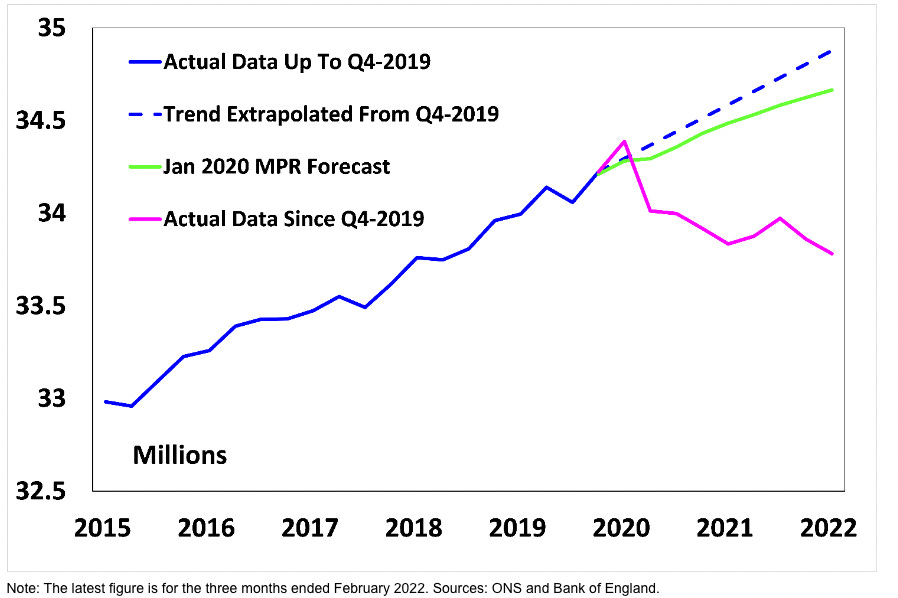

The workforce has shrunk by 440,000 people (1.3%) since Q4-19, and is 2.5% below the January 2020 forecast. The scale and persistence of this drop in labour supply has been a surprise to many forecasters, including us. The interplay between Brexit and the pandemic has reduced net inward migration (and hence population growth), while participation has fallen markedly (especially among people aged 50-64 years). Since Q4-19, the number of people aged 16-64 years that are outside the workforce and do not want a job has risen by 525,000 (1.3% of the 16-64 age population). This largely reflects increases in long-term sickness (roughly 320,000 people) and retirement (90,000), with smaller contributions from lower participation among students (65-70,000) and short-term sickness (30-35,000 people). The share of the 16-64 population who are outside the workforce and do not want a job because of long-term sickness is a record high, with an especially sharp rise among women (see figure 6). I suspect much of this rise in inactivity due to long-term sickness reflects side effects of the pandemic, for example Long Covid and the rise in NHS waiting lists.

Chart 8: UK – Workforce (Millions of People)

Source: BOE

Chart 9: % of Adult Population Aged 16-64 Who Are Outside the Workforce and Do Not Want a Job Because of Long-term Sickness

Source: BOE

He also suggested that Covid may have lowered the trend rate of growth further:

The economy’s potential output may have been further reduced since Q4-19 by weakness in business investment and adverse effects from Brexit on productivity. Moreover, changes in the composition of labour supply and spending (in terms of sector, skills and geography) may have exacerbated mismatch between supply and demand in the labour market.

Given the speed at which things have evolved since Covid it’s not clear whether these people have permanently left the labour force, or will come back over time as potential health issues are resolved. It is possible that impact on the net migration from Brexit is more structural now and could persist resulting in tighter labour markets.

However, it isn’t clear to me how raising interest rates to slow the economy helps with any of these factors. In fact, tighter labour markets could further encourage migration for skilled workers and also encourage people back into the labour market.

Unlike the US, where it’s possible to make a reasonable argument that they overstimulated, the same argument can’t be made in the UK. Michael Saunders also discussed this where he compares the size of the economy prior to 2019 versus right now:

At first glance, it may seem surprising that domestic cost and capacity pressures have escalated so much, and the labour market is so tight, given that real GDP is only slightly above the Q4-19 level. If potential GDP had grown in line with its pre-pandemic pace (around 1½% YoY) since Q4-19, then one would expect the economy to still have some slack.

However, since Q4-19, the economy’s potential output has fallen well below its previous trend.

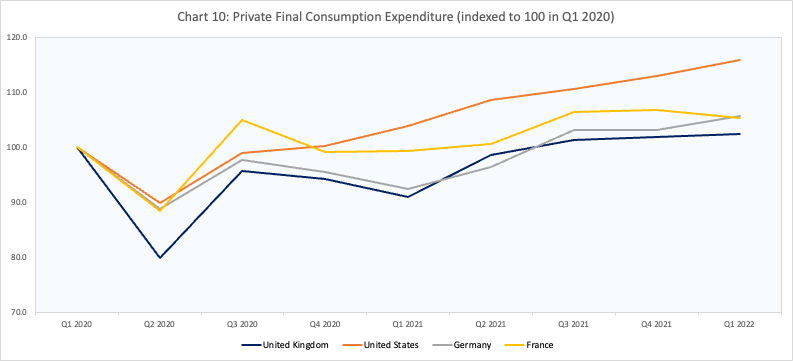

We can also look at Private Final Consumption Expenditure in the UK, US, Germany and France, which shows demand in the UK has lagged:

Source: FRED, VKMacro

Service sector inflation

Given the shock to both energy prices and sterling, it seems a given that the price of goods will rise, especially in the UK, where imports play such a large role. However, another factor Michael Saunders referred to in his speech was the inflation seen within the Services sector. He states that:

But the rise in inflation has become more broad-based, and partly reflects domestic cost and capacity pressures, because the recovery in activity has exceeded the economy’s potential supply. Capacity use in firms is well above average. The labour market is very tight – and has continued to tighten in recent months – with elevated readings for firms’ recruitment difficulties and a high level of vacancies. […] the rise in core services inflation – which is relatively less affected by global factors – points to the role of domestic factors.

Chart 11: Inflation within the services sector continues to rise

Source: BOE

The Bank hope that by raising interest rates, they can tighten financial conditions enough, and also reduce inflation expectations so that the domestic market can ease enough without causing a major downturn in the economy.

Michael Saunders is a bit more hawkish than Huw Pill, as his main worry is rising longer-term inflation expectations which are now at c. 4.5% using both surveys and financial market break-evens.

Source: Bloomberg, VKMacro

I’ve always found the inflation expectations view of inflation to be a bit spurious. In my experience, wage pressures rise when demand for labour increases due to faster economic growth, or worker union power strengthens helping bargaining power. I don’t see any of these things happening today, bar a small reduction in total labour supply due to Brexit.

Another factor to keep in mind is that the Government is a monopsonist employer of labour in many industries. Per the ONS, more than 5 million employees worked for the public sector at the end of March 2022, which is roughly 15% of total payrolled employees. The UK government has already announced their intentions to ensure public sector pay remains capped, so there’s no reason to see this changing anytime soon.

As Michael Saunders articulates, there are currently pressures in the services sector, but it’s unclear how much of this is temporary shifts in demand from goods to services and how much of this will be long lasting. From the Bank’s perspective I think they need to be seen to act and move in the right direction given where inflation is and the timidness of their reaction function in recent months shows their nervousness about the economy.

The difficulty for markets in this environment is that give the lack of forward guidance and the very clear inflationary pressures, it leaves an unclear picture of where the terminal rate is.

We saw a rapid re-pricing of expectations over the course of this year but as the weakness in the economy has become more evident, we’ve started to see a lower terminal rate. For example, looking at December 23’s Sonia futures, we can see the terminal rate has retreated from c. 3.4% around 20th June to 2.5% now (6th July). This means the market is no longer expecting meaningful hikes past September 2022 where futures continue to price in a rate of 2.2%.

So what does this mean for markets, and are there any investment opportunities?

Typically, the release valve for a weaker UK, and global economy would be to go short Cable (GBPUSD). This is especially true during idiosyncratic periods of weakness/ stress in the UK (e.g. during the Brexit vote). However, the currency has already moved to such as significant degree that the risk-reward to entering a new short Sterling trade is pretty poor. At the start of the year, I had a target of 1.20 to the dollar and we’re already way below that now.

Source: Koyfin, VKMacro

There are other places to look however. The recent shock to household incomes severely pressures the narrow areas of spending we saw occur during the pandemic. I think retailers in particular will come under severe pressure from both sides as slowing demand is coupled with her prices which pressure margins.

We’ve already seen this begin to play out as Asos PLC, one of the UK’s largest fashion retailers put out a profit warning where they said that:

Gross sales accelerated, however net sales were impacted by a significant increase in returns rates in the UK and Europe towards the end of the period, reflecting inflationary pressures on consumers which has a disproportionate impact on profitability

What is now clear, based on the significant increase in returns rates that we have seen, is that this inflationary pressure is increasingly impacting our customers shopping behaviour. It is too early to tell for how long the current pattern of customer behaviour will continue

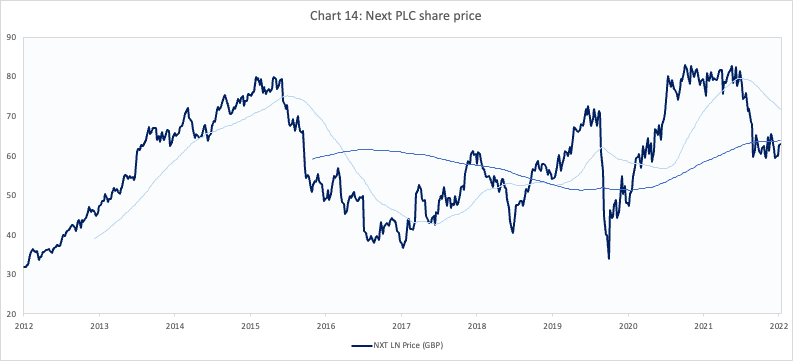

I think this trend is likely to continue over the coming 12 months. A company where these expectations don’t look to be fully priced in is Next PLC. Next is a omni-channel retailer in the UK, which has benefited from the pandemic. They’ve seen rising margins as a greater % of revenues came from online, and they faced lower costs from in-store due to the pandemic lock-downs. The Company also likely benefited from households accruing excess savings during the pandemic which meant that their target market expanded as more households were able to afford their clothing.

These tailwinds are set to flip the other way as lower disposable incomes mean that there’s likely to be less discretionary spending on clothing, and particular less from those on lower incomes. I believe there’s an opportunity here still as during Next’s recent earnings call, they re-affirmed their full-year guidance following the start of Russia’s war on Ukraine.

The CEO of Next stated that:

In terms of how that growth of 5% pans out over the year or how we're expecting it to pan out over the year, we're expecting the first quarter to deliver growth of around 21%. Q2, 0% as we come up against the sort of euphoric period of reopening last year and then 1% in quarters 3 and 4. I should stress at this point that it is particularly difficult to forecast the next 3 quarters' trade. And there is an argument so that actually Q3 and Q4, given all of the pressures that are likely to amount in the economy, could be worse than Q2.

The only thing that's weighing against that -- well, there are two things weighing against that. The first is that we anticipate we will be much better stocked in quarter 3 and quarter 4 than we were last year. And the other thing to stress is that these are nominal growth, these are the growth in pounds in the till. And of course, in real terms, particularly if wages have moved forward 4% or 5%, then we're looking at a real decline, particularly in those latter quarters of the year. So I think the important thing to stress is it's very difficult to look forward, but the numbers we're seeing at the moment would -- are in line with the plan that we set at the beginning of the year.

The other risk that could occur is that Next could find themselves with excess inventory come Q3-Q4 this year as they over extrapolate recent trends and find themselves over-stocking. We’ve already seen this dynamic occur in the US with some of the larger retailers such as Target and Walmart.

While Next’s share price has sold off since the start of the year, we’ve seen limited declines since, and the shares have been trading in a c. £10 range. I think there’s decent risk reward in shorting shares in Next if we were to head towards the top of the range at £65, with a target price of £45 - £50 (stop at £68). This further leg lower is likely to be driven by weaker than expected earnings, and a downward revision of the Company’s end of year target.

Source: Koyfin, VKMacro

Chart 15: Next PLC earnings estimates

Source: Koyfin

Another area where there’s likely to be a short opportunity is in UK banks. Typically, UK banks benefit from a higher rate environment. We can see the correlation in the relative outperformance of NatWest PLC against the FTSE 100 between the yield on 10-year Gilts below:

Source: Koyfin, VKMacro

However, this correlation only exists because typically, longer term rates rise when growth is accelerating. This time however, we’re seeing a higher rate environment at a time when real growth is set to decelerate, or even go negative.

During the recent earnings call, NatWest’s CEO discussed how they were yet to see signs of a slowdown in the economy. Relevant quotes below:

But we have a predominantly secured book. We're not seeing any signs of distress. And so a lot of what we're doing is actively managing knowledge and support and help for businesses and consumers deal with, what are different trends for them.

And what we've seen is a relatively low pass-through of that in terms of the early rate rises that we've seen come through so far. But in our underlying business, we're seeing continued strong mortgage growth and capacity to grow on that side of the book.

To me, the risks are that we see limited loan growth going forward, a reduction in housing activity as higher rates cut into the housing market, and higher delinquencies. NatWest have discussed previously that their loan book is the most sensitive to changes in UK rates so they seem to be a better placed short than a competitor like Lloyds Bank.

I think shorting NatWest at/ near current prices (£2.13) with a target of £1.84 which is near the lows as the war broke out makes sense.

It is worth noting that these single stock ideas are just initial screens for the broader UK post and further work would be required before entering into any position.

Hope you found this post useful.

Thanks,

VKMacro.