#7: A sluggish economy, but roaring industrials – what’s driving this discrepancy?

Despite leading indicators showing the industrial sector to be in contraction, industrials continue to outperform the broader market.

Summary:

Demand remains strong allowing industrial companies with pricing power to benefit

Supply chain issues are improving but remain persistent

Large backlogs should provide businesses with time to weather any periods of weaker demand

The investment opportunity is likely to be on the short-side going forward, but not yet

Since June 2022, the US Industrials sector ETF ($XLI) has outperformed the S&P500 by almost 13%.

What makes this more interesting is that during this period, we’ve seen an array of negative headlines hit the market such as a severe industrial recession in Europe, the on-going zero-covid policies in China and the slowdown in US housing driven by higher interest rates.

You would be forgiven for thinking of industrials, who’s revenues tend to be more sensitive to the economic cyclical, as a short or an underweight allocation in this environment, but it just hasn’t worked out.

Also, I get it.

Not every company within the industrials sector will be cyclical. Some of the largest companies by weight within the sector operate within Defence (i.e. Raytheon Technologies or Lockheed Martin), Professional Services (i.e. Verisk Analytics) and others.

However, even when focusing on the more cyclical areas such as businesses which operate within Machinery, Electrical Equipment, we’ve still seen broad outperformance.

Now part of this is obviously index specific and linked to weakness within the larger-cap tech names, but I’m more interested in investigating industrials strength.

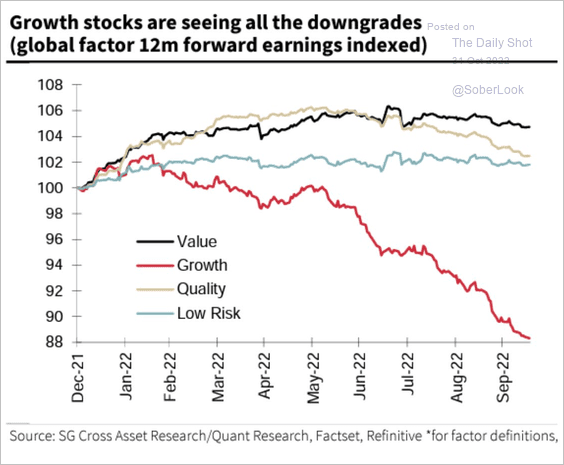

Chart 1: Growth stocks are seeing all the downgrades despite signs of weaker economy

Source: Société Générale Research

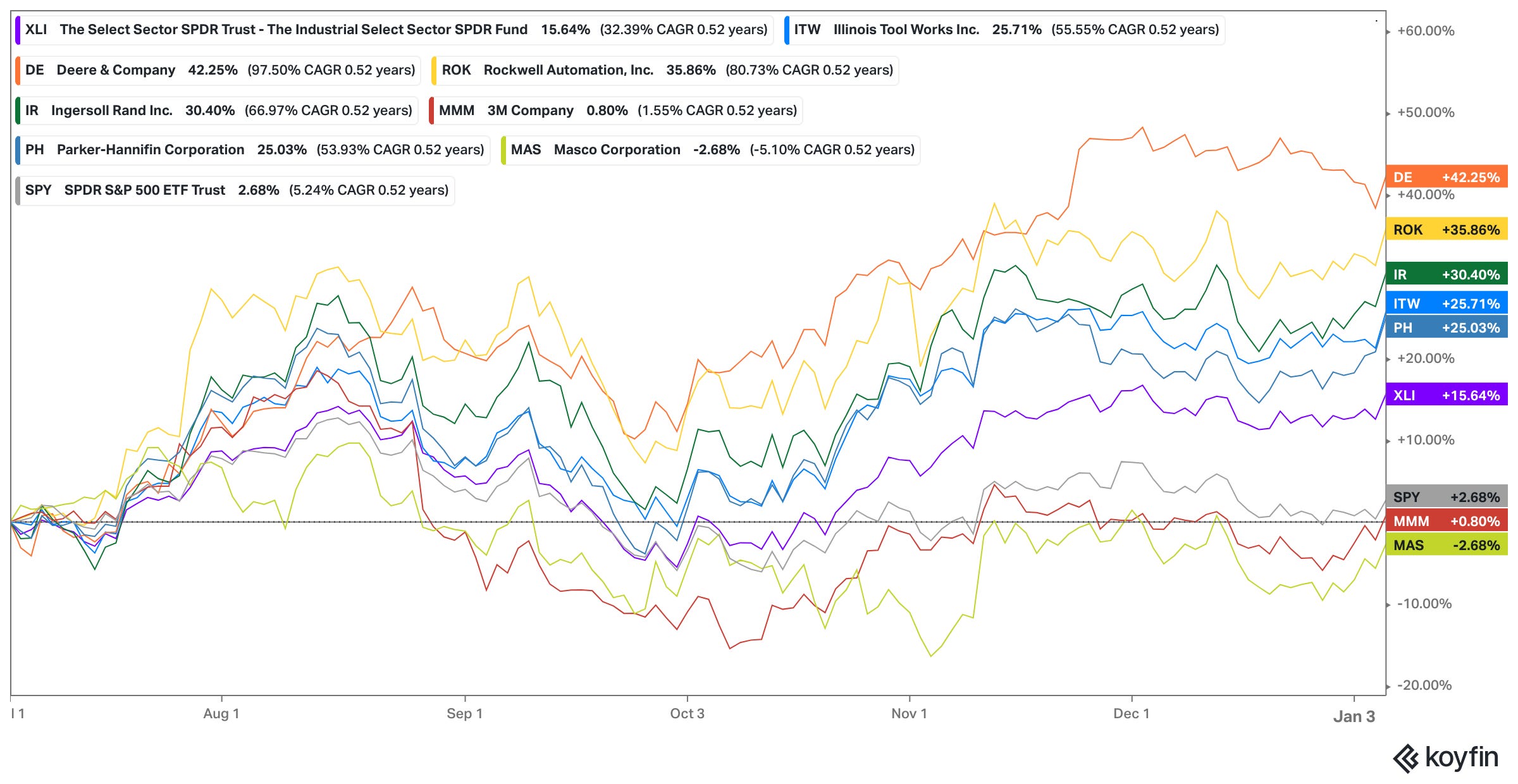

Using Caterpillar as the stylised example, and the ISM Manufacturing index as a proxy for the industrial cycle, I’m going to talk through what I mean.

As the ISM Manufacturing index rises, signalling increasing demand for industrial goods, so does Caterpillar’s share price in Y/Y terms. Also, what makes this more interesting, is that both the change in the share price, and the ISM typically leads actual business improvement.

The same can be seen on the downside, as demand begins to slow, we typically see Caterpillar’s share price fall in Y/Y terms as the market recognises the prospect of deteriorating revenues ahead.

Chart 2: Caterpillar’s share price and revenues are usually tied to the economic cycle

Source: VKMacro, Koyfin

We can see more recently however, that Caterpillar’s share price has begun rising on a Y/Y basis, even as manufacturing activity continues to wane. Also, revenues are no longer decelerating, and in fact are fairly stable.

In order to look into what has happening more deeply, I compiled a basket of industrial businesses which operate within the more cyclical areas to analyse.

The basket can be found within chart 3.

Chart 3: All but 2 stocks within the VKMacro Industrial basket has outperformed the S&P500 since June 2022.

These 9 businesses have been carefully selected based on their sensitivity to the cycle, and to ensure a broad coverage of end markets and regions. In order to conduct this analysis, I go through the each of the drivers of operating profit and the contributing factors impacting any change.

Revenues (Demand)

Theme 1: Overall demand remains strong.

Chart 4: Revenue growth accelerated in Q3 despite weaker leading indicators

Source: VKMacro, Koyfin

Total revenue growth for the basket has accelerated by 80 bps from 11.2% Y/Y in Q2 to 12.0% in in Q3 on a TTM basis, even has leading indicators have softened. When just taking a simple average of the basket, revenue growth accelerated from 10.9% to 11.1%. Deere and Caterpillar saw the strongest revenue growth in Q3, with only 3M seeing lower revenues relative to Q3 2021.

The overwhelming theme coming through when reviewing what these companies have been saying is that overall demand so far hasn’t fallen off, and instead has remained strong.

For instance, Caterpillar stated that they saw double digit growth on a Y/Y basis in each of their 3 key segments; resource industries, energy and transportation, and construction. One of the key drivers was the push towards sustainability which benefited a number of firms within the basket.

The resurgence in oil and gas demand has had a positive impact on Caterpillar, as the company is involved in a significant portion of the LNG value chain. Caterpillar's drilling and gas gathering equipment are in high demand, particularly in light of the United States' efforts to increase LNG exports.

Caterpillar also play an important role in helping with the provision commodities such as copper, nickel and cobalt required to produce EVs – a tailwind which is likely to benefit the company for some time.

Other sustainability initiatives are helping too, such as the revamp their existing machinery to ensure they’re more energy efficient.

We will replace 1 of the industry's largest mixed fleet that is currently comprised of over 160 haul trucks with new Caterpillar 798 AC electric drive haul trucks. Deliveries begin in 2023 and will extend over 10 years. The new electric drive trucks will feature technology that delivers significant improvements in material moving capacity, efficiency, reliability and safety.

Sustainability initiatives have benefited other firms too. For instance, Ingersoll Rand produce a broad range of compressors, vacuum and blower solutions as well as industrial technologies such as power tools and lifting equipment. They report that following the sharp increase in natural gas prices in Europe, a step change in demand could be seen for their compressors which provide cost savings via efficiency gains in just one year.

Similarly, Trane Technologies also recognised an increase in demand for their Thermo King HVAC unit following the European energy crisis. The Thermo King is a hybrid electric model which provides 30% fuel savings versus existing products on the market.

They stated that:

Energy efficiency, decarbonization and sustainability megatrends continue to intensify and create record levels of demand for our innovative products and services.

Lastly, Rockwell Automation reported double digit growth emphasising end demand in the US as Hyundai Motors selected Rockwell as their controls partner for press, body, paint and general assembly as part of their new Georgia based EV plant.

Theme 2: The market is laser focused on pricing power.

Something that became obvious very quickly when reading earnings transcripts is that the market is laser focused on which firms have pricing power thus being able to pass on higher costs to their end consumers, and which cannot. Each company was pressed repeatedly on what % of their revenue growth was due to unit growth, and what was due to price increases.

Caterpillar noted that c. 62% of revenue growth relative to Q3 2021 was down to price increases, with unit growth contributing 53% (-15% contribution from FX). 3M confirmed they were able to offset a lot of the inflation they experienced with mid-single digit price increases.

A number of these businesses don’t like to disclose price increases to the public as they’re often arrived to as a result of negotiation with long term customers. Illinois Tool Works being a good example here who saw revenue growth increase by 13% Y/Y relative to Q3 2021. When pressed further about how much of this growth was due to unit sales vs. price appreciation, they were quick to defend the strength of the end markets they were catering to.

In Q3, we saw meaningful volume growth across the company, including particularly in -- if you look at the strength in Auto, Food Equipment, Test & Measurement, you're not going to put out numbers like that without a meaningful contribution from volume.

Deere also reported that they were able to pass on large price increases to the end user and don’t expect this to change materially over 2023.

Theme 3: Backlogs remain abnormally large

The impact of the pandemic continues to impact these businesses as increased demand coupled with an impaired, but improving supply chain has resulted in the accumulation of large backlogs.

One of Caterpillar’s main customers are dealers who purchase their machinery and act as middlemen in various locations. Despite recent improvements, Caterpillar noted that on-going supply chain issues have resulted in dealer inventories remaining at the low-end of their historic range. Caterpillar’s total backlog continues to increase following Q3, as it grew by $1.6bn to $30bn in total.

Trane Technologies’ commercial HVAC business also saw an increase in backlogs now at unprecedented levels of $6.4 bn at the end of Q3 2022 which they expect to remain elevated until the end of next year.

Despite the size of the existing backlog being double the 20% of revenues it typically operates with, they have stated there are some benefits too.

The first is that larger than expected backlogs provides firms with extended line of sight, making planning and forecasting easier. The second is that should demand weaken in the future, they have more than enough work to ensure they don’t have to lay-off staff for a while until demand begins to rebound. This is particularly important given the difficulty most firms have had in hiring talented staff following the pandemic.

Deere was a standout in this area however, noting that order books remain full all the way to Q3 2023, with the order books for tractors in particular already 70% full. Even European order books are 65% full going into next year.

The risk with high backlogs is that you could see cancellations begin to rise as demand falls off. This is a pretty common phenomena in the semiconductor industry, where shortages lead to over-ordering. Eventually this results in supply gluts and cancellations.

However, this isn’t what’s happening. Yet.

Parker-Hannerfin noted that they’re yet to see cancellations materialise yet. Given the nature of their product and the limited competition they face, the company recalls that they’re usually able to negotiate with customers about delaying delivery dates rather than cancelling orders outright.

Rockwell Automation were also asked about cancellation rates given that backlogs are about 60% larger than usual. However, the general feeling was similar to Parker-Hannerfin. The message is that end demand remains strong, and cancellation rates remain at low single digits and within historic norms.

Theme 4: Residential housing and consumer electronics is beginning to soften.

Despite the environment generally being supportive, the impact of a shift away from goods towards service, and higher interest rates are beginning to bite.

Masco is a manufacturer and producer for home improvement products. Unlike a number of the businesses discussed so far, the firm saw declines in unit sales resulting in weaker than expected revenues despite increasing price by almost 9%. Moreover, the business says it noticed a material downshift in demand in September which was broad based and particularly noticeable in their DIY paint market. This weakening of demand also resulted in Masco being unable to push through the level of price increases they would have liked.

Just shifting to the Fed for one moment, this is exactly what they want to see. Interest rates directly impacting the housing market, which in turn slowly seeps into lower demand within the economy.

Illinois Tool Works also spoke about this in their earnings call. 20% of their revenues are generated in construction and housing. 80% of this is residential housing, while the rest is commercial. Interestingly, they saw weakness in residential housing across all geographies, including Europe and the UK. As mentioned before, housing is the most rate sensitive area of the economy, so it makes sense that this is the first area where we’d begin to see weakness. Like Masco, this weakness is impacting Illinois Tool Works’ pricing power within residential construction.

3M also noticed slower than expected revenue growth as changing preferences and inflation began to impact disposable income.

We expect the macroeconomic environment to continue to moderate while geopolitical uncertainties persist, impacting energy costs and end market demand, particularly in Europe.

I would say consumer spending continues to be weak. Even in the month of October, we have seen lower consumer spending. I called that out as those trends where the inflation is impacting the consumer, I think, remains through the holiday season as well as how inventory levels are adjusted by retailers is something that we'll have to watch.

Theme 5: A strong dollar was a headwind across the board.

Another consistent theme was the negative impact a rising dollar had on revenue growth. The reasoning here is simple, as most companies here earn a large % of their revenues abroad, a rising dollar reduces the value of these revenues when converted back to dollars.

The impact of the rising dollar also varied company by company, depending on what % of revenues were generated abroad, and also what % of costs were non-dollar based.

The table below provides the impact on revenues on each Company. It’s worth noting that since the end of October, it looks like the dollar may have peaked. Therefore, its now acting as a headwind to industrial earnings from the headwind we’ve had thus far.

Table 1: A stronger dollar acted as a headwind to revenue growth

Source: VKMacro, Company Transcripts

Cost of Goods Sold

Theme 1: Commodity and freight costs are beginning to fall.

2022 was characterised by a rapid increase in prices across the board. Inflation was broad based, and felt in particular by firms buying and using raw materials as inputs into their production process. Most industrial companies use base metals such as steel, copper aluminium as well as semiconductors which have been in short supply.

The impact of this rapid increase in prices has been to put downward pressure on gross margins, thus hurting the valuation of most businesses (especially when combined with the discount rate shock – thanks Fed!).

Chart 5: Despite lower commodity prices, costs remained stubbornly high

Source: VKMacro, Koyfin

However, Q3 was the first real time a number of firms began to comment on the fact that prices were no longer going up at the rate at which they have been thus far.

Lower commodity and freight costs began to feed through.

Here’s what Caterpillar had to say in response to a query about lower freight costs:

Material and freight costs have increased by about 20% since 2020. Our gross margin of 28.5% for the third quarter is now only just getting back in line with the levels seen in the third quarter of 2019, despite sales and revenues being higher.

I mean actually, the biggest single factor that we are focused on rather than actually just pricing freight at the moment is actually utilization of freight because one of the challenges has been actually the amount of freight we've had to use in order to get components around to actually build machines. That's been probably the bigger driver of some of the increase that we've seen.

The second part is, yes, you are correct, freight spot rates are coming down. We tend to contract normally 6 to 12 months in advance. So we have not yet seen the benefit of those low rates. And those low rates are some things we are favorable on. For example, roll on, roll off, we're actually favorable to the current market.

But obviously, container freight is coming down as well. So we're seeing some favorability on that in the spot market. Obviously, we'll expect some of that to flow through as we move into 2023.

I think this is helpful in allowing us to understand why inflation is typically such a lagging indicator. Even when freight costs for example come down, it typically takes time to feed through the system and begin to benefit the end consumer. Caterpillar discussed the typically contract length of 6 to 12 months above, and it is likely similar for most businesses.

For a company like Illinois Tool Works, commodity prices are a particularly large input into production. They estimate it at roughly 60 to 65% of total cost of goods sold, with the remaining being freight, labour and other elements.

Deere also commented on the fact that they’re beginning to see freight costs come down and particularly called out the lower price of steel as well. However, labour continues to remain a challenge, as does energy costs.

A particularly interesting comment on labour availability came from Parker-Hannerfin who stated that:

But for me to tell you that labor availability is still a non-issue, I would be kidding you. It's still a little bit a deal. I think the thing that helps us through a lot of this is we just use our Parker lean system, and we go in and we just figure out how we're going to reconstruct the value stream and bring out the efficiencies and get better throughput, et cetera.

It’s worth noting that the issue with raw materials wasn’t just around higher prices, it was also about the lack of supply and delivery. Here’s 3M providing further colour on the evolution of costs and commodity supply.

What we are seeing is a little moderation in inflation, but it's not been consistent and persistent. We are seeing inflation is pretty much still broad-based.

However, if you look at intermediate finished goods, they are still pretty high and so is specialty raw materials. So I would say if you just look at what inflation we had in the third quarter, it was $225 million. In the fourth quarter, we are seeing somewhere between $100 million to $150 million. So there's a little moderation.

We are seeing raw materials flowing a little better than it has flown in the prior quarters, and you can see that's why the team was also able to deliver decent productivity in Q3.

Theme 2: Supply chains are on the mend.

For those of you who follow the ISM Supplier Delivery sub-index will know that delivery times have been falling for 3 months in a row now, having risen rapidly since the onset of the pandemic.

Don’t forget, this sub-index measures the rate of change of delivery times, rather than providing the absolute level. In reality, true supply chain normalisation is likely to require a much longer timeframe of falling delivery times.

The semiconductor situation also remains complex. Certain areas within the industry are seeing oversupply such as DRAM and NAND but this is not the case across the board. Caterpillar for example are yet to see any meaningful improvement in supply which continues to hurt the rate of production.

Another impact of supply chain disruption is that firms typically run with higher working capital as they look to pull various shorter-term levers to mitigate the impact of the disruption. A study by PwC Germany found that net working capital as a percentage of sales has risen since the pandemic began, and this trend continues to persist. The main example of this that firms is that companies may need to maintain higher levels of inventory to account for longer lead times and uncertainty in the supply chain.

The evidence presented in this paper matches 3M’s experience who have been running with higher-than-usual levels of working capital, but now expect this to come down over 2023. You can see this when looking at their days of inventory outstanding which is currently sitting at just under 100, from a pre-pandemic average of 90.

Here are a couple of quotes just summarising how firms are currently feeling about the supply chain:

Rockwell Automation:

Our planned inventory reductions did not materialize in the quarter due to the continued build of raw material and work in process waiting on critical components. Our inventory days on hand at the end of the current year were close to 130 days versus a pre-pandemic average of 90 to 100 days.

Parker-Hannerfin:

Yes, supply chain is healing, but I would say it's healing slowly, and it's not really making, I would say, that big a difference on lead times, at least not yet.

Theme 3: Supply chain issues directly impact productivity.

One of the issues with operating in an environment of supply chain issues is that it directly impacts a firm’s efficiency and therefore its productivity. We can see this in the macro data. Productivity within the manufacturing sector fell in y/y terms during Q2 and Q3 this year.

There have been a number of theories about why this might be the case, some which could make sense such as the rapid pace of hiring that’s taken place since the pandemic recovery meaning workers need to be re-trained, thus adding to hours worked but not output. Other less reliable theories are things like ‘quiet quitting’ or work from home.

I like to tie things back to real life constraints. The best example of how productivity is impacted was given by the CEO of Trane Technologies. His comments below.

I think one of the knock-on effects of the supply chain that's inconsistent is productivity, right? So if you think about you're running a factory, and you don't have the right components, you're stopping lines, you're partially building product, you're putting it out in the yard, you're bringing it back on the line when you get the components to retest the product because, obviously, you want to test everything before it gets shipped out to a customer. So it's been disruptive. It's improving, but it's going to improve slowly as the supply chain improves.

This example is pretty consistent across the board and is something which has also impacted the automotive industry writ large, as they wait for specialist parts and semiconductors for example.

The bull case here, which the market is pricing is that margins re-accelerate next year as the impact of lower costs continue to benefit these businesses, particularly those which are more sensitive to commodity prices.

However, this benefit only really applies if demand continues to hold up. In Masco’s situation, declining sales volumes meant that it continues to take longer than expected to run through raw materials, thus taking longer for lower commodity prices to feed through the firms PnL.

Gross profits

Tying the key themes discussed thus far together, we can understand why gross margins peaked in Q2 2021 (incidentally also when industrial companies began to underperform the broader market), but also why it looks like they’ve troughed in Q2 2022.

Chart 6: The trend of decelerating gross profit growth reversed in Q3

Source: VKMacro, Koyfin

Chart 7: Gross margins began to expand in Q3 and should continue to do so into Q4 and possibly Q1 2023

Source: VKMacro, Koyfin

Of the 9 industrial companies selected, only 3 saw lower gross margins in Q3 2022 relative to Q2 and 4 companies saw gross profits decelerate Y/Y since Q2.

It’s important to understand that given the abnormal nature of the economy right now, most companies are not seeing quarterly results match pre-pandemic seasonal patterns. For instance, Caterpillar typically tends to report higher gross margins towards the start of the year, which slowly decrease, however this year we’ve seen the opposite.

Illinois Tool Works is an interesting example of this as well. They’ve suffered a 200-basis point hit to their gross margins due to the impact of costs rising faster than selling price (despite continuing to see strong demand). The company has hinted that that as long as pressures continue to ease going forward, they are looking to maintain gross margins at 42% as per historic guidance, which is an industry leading level.

SG&A

Chart 8: Higher labour costs are finally impacting SG&A costs as a % of sales

Source: VKMacro, Koyfin

Following almost 4 quarters of falling SG&A costs as a % of revenues, we saw a slight reversal in Q3 2022.

It’s worth noting that the majority of SG&A costs tend to be labour related and therefore less volatile. So as wages continue to rise at a fairly rapid pace, we should also see SG&A costs rise continue this rise as a % of revenues.

Recession fears however could force companies to cut back on marketing spend for instance in an effort to save cost. Masco discussed that they often look at SG&A as a lever which can be pulled depending on the growth outlook.

Operating Profits

Now putting everything together, we see that better than expected revenue growth, coupled with price pressures that are beginning to ease should leave this basket of companies with higher margins going into q4 earnings.

Chart 9: Faster than expected revenue growth hasn’t been enough to prevent the deceleration in operating profits

Source: VKMacro, Koyfin

Chart 10: Operating profit margins continue to be under pressure due to higher labour costs but this could reverse going forward

Source: VKMacro, Koyfin

The reality is that once supply chain pressures ease, a number of these firms will have likely built-up operating leverage having dealt with supply restrictions over the last couple of years.

Should demand hold up, then earnings will likely reach new highs again. That’s what the market has been pricing, especially with China reopening acting as a tailwind into Q1 2023. When you couple this with the weaker dollar we’ve seen as well it’s not difficult to see why these companies are at or close to new highs right now.

I think the bull-case is best articulated by the guidance provided by Caterpillar and Illinois Tool Works:

Caterpillar:

One of the things to keep in mind is that our margin targets are progressive, which means that we need to achieve higher operating margins as sales increase. And in a moderate inflationary environment, which we saw for many years, sales increases typically are led by higher volumes, and the benefit of the operating leverage associated with those higher volumes helps us achieve our progressive margins. In the environment where we are in today, where a relatively larger portion of the sales increase is due to price realization, there's less operating leverage, which makes the delivery of those progressive margins more challenging to achieve.

Illinois Tool Works:

We're expecting that if inflation stays where it is, and so based on the known increases and decreases and based on the price that we expect to realize in the fourth quarter, that price/cost will be accretive on an EPS basis and also, for the first time in a while, accretive on a margin basis as well. I think it's reasonable to assume that our incremental margins will be a little bit higher than our normal range, just given the recovery on price/cost that we talked about.

The big risk remains the demand picture. We shouldn’t forget that these are cyclical businesses and we shouldn’t risk buying them at peak multiples of peak expectations.

The bigger opportunity here is to monitor these companies going forward on the short side once there are clearer signals that the cycle is turning. What this exercise does tell us though is that it’s not likely to be during the next 3 months.

Summary:

Demand remains strong allowing industrial companies with pricing power to benefit

Supply chain issues are improving but remain persistent

Large backlogs should provide businesses with time to weather any periods of weaker demand

The investment opportunity is likely to be on the short-side going forward, but not yet

Thanks,

VKMacro