#11: Some questions on the cycle

#11: Some questions on the cycle

Some thoughts on what's preventing me from having more confidence about my view.

Questions:

How important are real income gains for consumers while small and medium-sized businesses are going to face more and more difficulty accessing credit?

Given real income growth is not only positive but accelerating, will goods demand be as weak in 2023?

How important is the divergence between input and selling price data in recent surveys? Is this a sign of more robust consumption and perhaps margin growth this year?

How high is the bar for the Fed to hike rates going forward, and can the market price-out-forward rate cuts given the banking issues we’ve seen?

When do the weak links in Europe begin to show cracks?

To the extent that I have an analytical edge, I believe my edge is having a better sense than most about the second derivative in growth and inflation.

Economists don’t think it matters much, they see current economic data and believe things are fine. While I share some of their optimism, I believe there are a number of areas they’re overlooking that are becoming incrementally worse on the margin.

The bears however continue to look at survey data for the manufacturing sector and proclaim ‘doom is upon us’. It’s just a matter of time before everyone else realises it.

No surprises there. But again, some of their arguments have merit, and we should be agnostic and open when considering our body of evidence.

So this time there isn’t a coherent view being presented but a series of questions accompanied by conflicting data which I hope conveys some of the factors I think are most important right now.

Question 1: How important are real income gains for consumers while small and medium-sized businesses are going to face more and more difficulty accessing credit?

This cycle has been defined more by income gains rather than credit growth. It first started with the outsized fiscal package in the US but was also supported by the part-closed economy we all faced over 2020 - 2021.

This led to a large body of savings being built up while income growth for those on the 1st and 2nd wage quartiles has been the fastest growing further supporting demand.

However, any excess savings are now most likely being held by solely higher earners, who have a smaller marginal propensity to consume. Excess savings held by those on lower incomes are likely to be spent.

Don’t believe me? Well, the evidence is in the data. If excess savings were still a driving force, we wouldn’t see real personal consumption decelerate at the pace we have.

It is not just goods demand that’s struggled, but services too. Real PCE growth in services is now growing by 2.4% Y/Y, and c. 0.3% over the last 2 quarters on a 3m/3m basis. Nothing to write home about.

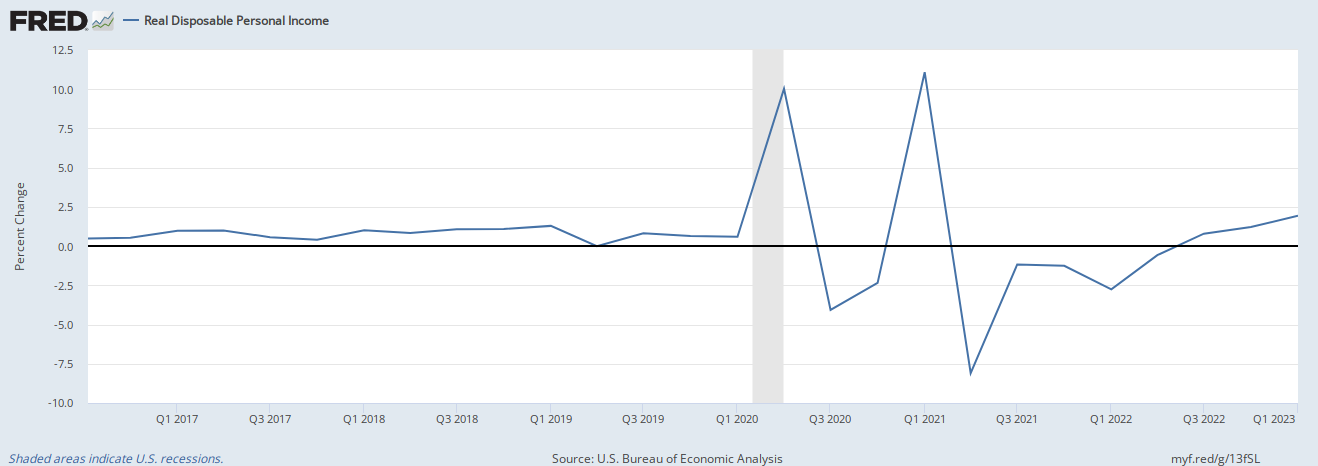

So what’s the conundrum? Well, it goes something like this. Real disposable income growth has been accelerating - now growing at c. 4% Y/Y, and c. 2% on a 3m/3m basis - something I flagged in February. This should further support consumption going forward as the pressure faced by consumers over 2022 from high gasoline and energy prices fade away.

At the same time, the issues stemming from the US banking sector are likely to hurt loan growth, especially in small and medium-sized banks. In my view, this impacts smaller businesses, commercial real estate (broad basket - although only office spaces are a worry for now), and energy firms the most.

In addition, broader goods demand is still weak, and a real source of risk to the economic cycle. We’ve seen a host of companies discuss this from electronic goods manufacturers, Maersk, JB Hunt, and more.

How these factors interlink will be the defining factor for the rest of this cycle. At the moment, we don’t have enough information.

Question 2: Given real income growth is not only positive but accelerating, will goods demand be as weak in 2023?

Real income growth was negative over most of 2022. Russia’s war on Ukraine made the pain worse, and when coupled with a shift in demand preferences, the consumer goods sector, particularly electronic goods (where bullwhip was most severe).

As mentioned above, if real income growth is now positive and rising, and if unemployment continues to stay low - how likely is it that consumer goods demand doesn’t rebound this year?

We’ve seen early signs already in the latest S&P surveys - where the consumer goods PMI went from slightly negative to more to a 53 level indicating growth.

If we do see a rebound in goods demand - we’re likely to lead a rebound in the manufacturing sector, the semiconductors industry (memory, CPUs, etc.), and industrials metals.

Memory stocks in particular look cheap and could be a reasonable way to benefit from any rebound.

Also, note the weakness now registered within Financials. This speaks to the difficulty in assessing the path forward.

Question 3: How important is the divergence between input and selling price data in recent surveys? Is this a sign of more robust consumption and perhaps margin growth this year?

The ISM survey is great, but it doesn’t offer the granularity in certain areas as other surveys. For instance, price pressures are discussed from an input perspective only.

Other surveys such as S&P’s PMI or the Regional Fed surveys offer a bit more granularity and are starting to show a more and more consistent trend.

Output prices are rising, even as input costs are stable/ still falling. This points to margin expansion ahead, something that will support equity multiples if it materialises.

The other side of this is inflation remains sticky, and assuming the economic landscape looks more benign, rate hikes come back on the table.

Question 4: How high is the bar for the Fed to hike rates going forward, and can the market price-out-forward rate cuts given the banking issues we’ve seen?

A bit more market related but this question is more self-explanatory.

Chair Powell teased that the bar to further rate hikes is now higher than it has been. They expect to see credit standards tighten materially among small and medium-sized lenders and they’re not sure how big this impact will be.

Even Bullard who’s leaned more hawkish than other members over the last year hinted at something similar.

So the question is how high is the bar for upcoming data to cause the Fed to shift, and how long are they willing to wait before being more comfortable about the impacts of reduced bank lending?

I don’t think we know yet - but there is a market implication too.

Given the issues the banks have faced, why would the market fully price out rate cuts over a 6-month window going forward? For now, I don’t think it does, which should cap the downside in long-duration fixed income and therefore prove to be bullish for long-duration equities.

Question 5: When do the weak links in Europe begin to show cracks?

The UK and Sweden in my view are the weakest links in Europe right now. Incoming data looks poor, and both economies should see the impact of tightening significantly impact consumers via higher mortgage payments from Q3 onwards.

There is a flip side, gasoline (petrol) prices have come down, and have further to go in Europe. In addition, utility bills and food prices should provide a material tailwind to lower-income consumers.

How much do these factors offset each other? How much risk are the Riksbank and BoE willing to take before deciding to wait until they have a better read of the impact of their tightening?

We don’t know yet - but if cracks are going to appear in Europe, it is likely these two economies will be at the forefront. Sure, Germany could also suffer on the back of weaker manufacturing demand and other economies may also be at risk due to weaker housing activity. No arguments there, but I suspect record backlogs sustain industrial employment for some time and the mortgage passthrough isn’t at the same level.

So unfortunately, I don’t have many answers for you this time, but I do have a tonne of questions. If you have some thoughts on some of these matters let me know!

Thanks,

VKMacro